Choose Debt Funds Wisely

We prefer investments like PPF and NSC that offer assured returns. But interest rates in small saving schemes are on a downward trend. The annual interest rate on PPF has gone down to 7.1% and on the 5-year National Savings Certificate to 6.8%. Debt funds can provide better returns and are more liquid. They are less risky compared to equity investments. Therefore, they can play a significant role in your investment portfolio. Investors are wary of debt funds due to some schemes being closed abruptly and investors being denied redemption. But we cannot dismiss debt funds due to a few stray incidents. Many debt funds manage money well and give optimum returns.

Should I invest in debt funds?

Interest rates on fixed-income investments are at their lowest in the last 30 years. Debt funds score over them in many aspects -

- More tax-friendly than bank deposits. You pay annual taxes on interest accrued on deposits but on debt funds only when you sell them.

- Short-term sales proceeds of debt funds are taxed as per your income tax slab. If you sell after three years, you pay a 20% tax after indexation. Your tax outgo is lower.

- You get money within 1-2 working days on the redemption of a debt fund. It is a highly liquid investment.

They are a good alternative to fixed-income investments in the current scenario.

As an investor, understand that different debt funds have different characteristics and each has a different risk-reward ratio.

Types of Debt Funds and Key Risks

There are 16 types of debt funds. Each is different in terms of tenure of investments, and type of securities invested in. They have different risk-levels based on underlying securities, duration, and interest rates. Check the following before investing in one -

- Investment objectives

- Relevance to your portfolio

- Risks

- Investment cost

- Tax liability

- Potential returns

Key Risks and Risk Mitigation

Let us look at the inherent risks of debt funds and how to mitigate them -

Credit Risk

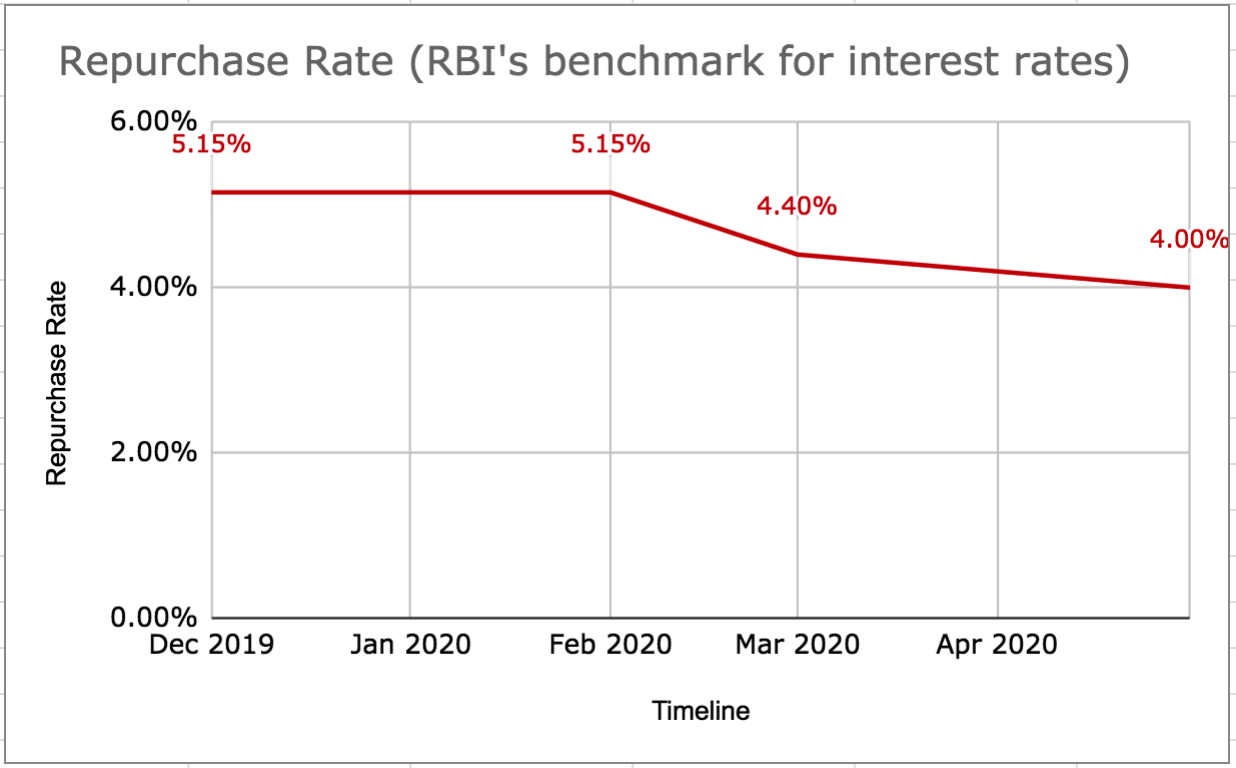

Credit risk is the risk that the issuer of an underlying security defaults on either interest or principal payment or both. Credit-rating agencies assign ratings to debt instruments. The higher the rating, the safer the instrument. For example, an ‘AAA’ rated bond is safer than an instrument with rating C. Interest rates are dependent on the RBI’s repurchase rate. The chart below shows that this has been falling for some time now -

This can lead some schemes to invest in riskier instruments for better returns leading to chances of default.

Mitigation of Credit Risk

Debt fund managers manage the portfolio such that risk is minimal. AMCs evaluate investments and bond issuers. They diversify across instruments and issuers. They demand collateral for risky investments and analyse if money borrowed is used for stated purposes.

As an investor, avoid funds with high credit risk. Check ratings of the underlying securities. Evaluate the portfolio of your debt scheme. Higher allocation to risky instruments, significant investments in volatile sectors, or overallocation to a particular security are signs to steer clear of the fund. Keep track of the fund management and market news. If you are uncomfortable with returns or news, or have reached your financial goals, it is better to exit from the investment.

Liquidity Risk

Liquidity risk is the extent of the ability of the fund to sell bonds in the market. If there are many redemption requests in a debt scheme, but the MF is unable to sell the underlying bonds, it may not have enough money for redemptions resulting in non-payment to investors.

Mitigation of Liquidity Risk

Competent MFs manage inflows, borrowing, and investments such that they honour all redemption requests. They use the laddering technique whereby they invest in instruments that mature at different times to have a constant cash inflow. They have lines of credit with banks to tide over short-term illiquidity.

As an investor, invest in funds that have high-quality portfolios. Evaluate your investments regularly to reduce the chances of rude shocks.

Interest-rate Risk

Interest rates have an inverse relationship with NAVs of debt funds. Rising interest rates lead to a fall in NAVs, and falling interest rates lead to a rise in NAV. If the interest rate rises, existing bonds will have to pay higher interest rates, and they become less attractive. Funds with long-term bonds will be more volatile compared to funds with short-term bond holdings.

Mitigation of Interest-rate Risk

Mutual funds cannot always predict the interest rate movements accurately. So their portfolio should be well-diversified to absorb losses and manage large redemptions without the NAV falling.

Retail investors too cannot estimate interest rates accurately every time. They should invest in short-term and long-term duration bonds. Bonds maturing in 3-4 years are impacted less by interest rate movements compared to bonds of longer duration. Do not invest money you might need in the next 1-2 years in long-duration debt funds.

Conclusion

Choose the right debt fund by looking at its investment portfolio, returns and YTM values. Double check on schemes that have superior returns or YTM. They might be invested in low-rated securities that provide higher returns but increase the credit risk. Small but regular investments in the right debt funds will make your money work for you and earn you steady returns.

Vidya Kumar