Is gold a sensible or a sentimental investment ?

There are 2 primary reasons why you need to invest in gold. Investing money in gold is worth because it is the best hedge against inflation. Over a period of time, the return on gold investment is in line with the rate of inflation. It is worth investing in gold for a one more very valid reason. Gold is negatively correlated to equity investments. Say for example 2007 onwards, the equity markets started performing poorly whereas the gold has performed well. So having gold as an investment option in your portfolio mix will help you reduce the overall volatility of your portfolio. Its also serves as a means of easy liquidity in case of an emergency and urgent need for funds or for pledging as an asset ( Loan against asset ) .

Is it profitable to invest in gold? This investment proved remarkable from 2006 to 2011.During that time span Gold has given an average return of 29% per annum which was any day better than other investment options. However, the long term average return on gold investment is lesser than 10% p.a. As one can say technically or ironically but history always repeats itself. Therefore, we may once again observe the similar less than 10% appreciation pattern in gold prices in near future. A 5 % of the overall investment portfolio can be considered for gold investments (bullion, WGC coins, Gold ETFs). Jewellery is not an investment as far as personal finance goes. It does not appreciate as an asset. It is only an expense for pleasure, symbolizing wealth.

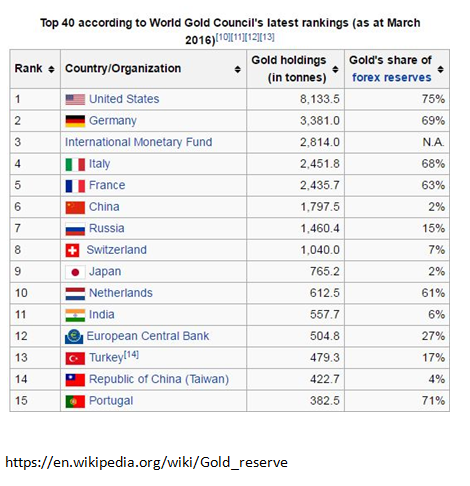

Research shows that over 16,000 tonnes of gold is there in Indian households predominantly in the form of jewellery. The value of this as per market price is a whooping Rs 27.2 lakh crore. That is close to twice the foreign exchange reserves held by the RBI. A gold reserve is the gold held by a national central bank, intended as a store of value and as a guarantee to redeem promises to pay depositors, note holders (e.g. paper money), or trading peers, or to secure a currency. The gold listed for each of the countries in the table may not be physically stored in the country listed, as central banks generally have not allowed independent audits of their reserves.

List of investment options and the mode of operation:

- Gold Sovereign scheme

- Gold ETF

- Gold monetization scheme

- Gold bonds

- Physical Gold

Gold Sovereign scheme :

The Government of India will be launching the Sovereign Gold Bonds Scheme soon. As investors will get returns that are linked to gold price, the scheme is expected to offer the same benefits as physical gold. They can be used as collateral for loans and can be sold or traded on stock exchanges. Sovereign Gold Bonds will be issued on payment of rupees and denominated in grams of gold. Minimum investment in the bond shall be 2 grams. The bonds can be bought by Indian residents or entities and is capped at 500 grams. The Bonds are issued by the Reserve Bank of India on behalf of the Government of India. The bonds are distributed through banks and designated post offices. This should make subscribing to the bonds an easy affair. During redemption, “the price of gold may be taken from the reference rate, as decided, and the Rupee equivalent amount may be converted at the RBI Reference rate on issue and redemption”.

Investors can apply for the bonds through scheduled commercial banks and designated post offices. NBFCs, National Saving Certificate (NSC) agents and others, can act as agents. They would be authorised to collect the application form and submit in banks and post offices.The Sovereign Gold Bonds will be available both in demat and paper form.he tenor of the bond is for a minimum of 8 years with option to exit in 5th, 6th and 7th years.They will carry sovereign guarantee both on the capital invested and the interest.Bonds can be used as collateral for loans.Bonds would be allowed to be traded on exchanges to allow early exits for investors who may so desire.In Sovereign Gold Bonds, capital gains tax treatment will be the same as for physical gold for an ‘individual’ investor. The department of revenue has said that they will consider indexation benefit if bond is transferred before maturity and complete capital gains tax exemption at the time of redemption.

Investors can apply for the bonds through scheduled commercial banks and designated post offices. NBFCs, National Saving Certificate (NSC) agents and others, can act as agents. They would be authorised to collect the application form and submit in banks and post offices.

The investors will be compensated at a fixed rate of 2.75 % per annum payable semi-annually on the initial value of investment.

Interest on the Bonds will be taxable as per the provisions of the Income-tax Act, 1961 (43 of 1961). Capital gains tax treatment will be the same as that for physical gold. (https://www.rbi.org.in/Scripts/FAQView.aspx?Id=109 )

Pl specify the objective of RBI doing this.

In India, demand for physical gold is amongst the highest in the world. This causes the government to import physical gold in large quantities which in turn is a drain on the foreign exchange reserve. Issuance of the SGB will help in reducing the physical demand and thus bring down the import bill for physical gold, considerably. The foreign exchange thus saved can be channelized to strengthen India’s economy.

Gold ETFs

Buying Gold ETF is purchasing gold in electronic form. You buy them just like you buy stock of any company from your broker. Gold ETF makes it easier for you to invest in gold. The investment objective of Gold ETFs is to provide you with returns that closely correspond with the domestic price of real gold. Each Gold ETF unit that you buy is roughly equal to the price of 1 gm of gold.

They are easy to buy since you can even buy just one gram at a time. Over time, you can build up your gold portfolio to the level you want, just as you would with your bank or jeweler, only this is easier.

Benefits:

The gold monetisation scheme earns interest for your gold jewellery lying in your locker. Broken jewellery or jewellery that you don’t want to wear can earn interest for you in gold.

Coins and bars can earn interest apart from the appreciation of value

Your gold will be securely maintained by the bank.

Redemption is possible in physical gold or rupees hence giving your gold purchase further earning opportunity.

Earnings are exempt from capital gains tax, wealth tax and income tax. There will be no capital gains tax on the appreciation in the value of gold deposited, or on the interest you make from it

The current rate of interest on a medium-term gold deposit is 2.25 per cent annually; for a long-term one, 2.5 per cent. The government, said the circular, might change these if needed at a future date. The lock-in period for medium-term deposits will be three years; for long-term ones, five years. The principal and interest rate on short-term deposits, essentially bank deposits, will be denominated in gold. Medium and long-term gold deposits will be treated as government borrowing.

For medium-term deposits, withdrawal between three years and five years will attract a penalty of 0.375 per cent in reduced interest rate. For withdrawal between five to seven years, the penalty will be 0.25 per cent in a reduced interest rate.

For long-term deposits, the penalty between five to seven years will be 0.25 per cent; between seven to 12 years, 0.375 per cent; between 12 to 15 years, 0.25 per cent.

For medium and long-term deposits in the first year, the government will pay banks a total commission of 2.5 per cent — 1.5 per cent as handling charges and one per cent as commission. This was a major clarification, without which banks were reluctant to proceed with accepting of deposits. “For the purpose of computing the charges and commission payable to banks, the rupee equivalent of the gold deposited shall be calculated based on the price of gold prevailing at the time of deposit,” RBI said.

The tax implications on GMS will be notified by the government from time to time, RBI said, adding the quantity of gold will be expressed up to three decimals of a gram.

So far, 2,820 kilograms of gold have been mobilised under the scheme

Drawbacks:

The gold can be deposited even in the jewelry form, but it gets melted and the value is determined after testing its purity. The depositor can choose an option to get back the gold at a later date in the equivalent of ‘995 fineness gold or Indian rupees’ as they desire, but not in the same form.

Since gold items held in GMS are not returned “as is where is ” basis but an equivalent form and quantity is returned , people are skeptic and sentimental about such gold deposit.

If subscribed fully in the first year, SGBs could result in saving of $2 billion on gold imports at current prices.

Tabular format differences between Soverregin Gold Bond Scheme and Gold Monitisation Scheme

| Physical form | Wastage and loss | Interest | Tenor | Redemption | Limit | Tax | |

| Gold sovereign bond | No physical gold to be bought or sold | No wastage or loss | 2.75%payable semi- annually | 8 years with lock in of 5 years | Prevailing value of gold as per rate published by IBJA | Max 500 gms per person per year | Income tax on interest & wealth tax |

| Gold Monetisation scheme | Govt will take possession of the gold | Wastage and loss due to melting and purity | 2.25-2.5% | 3 yrs – 5 yrs lock in | Gold / cash equivalent of the initial deposit | No max limit | No tax on interest |

Gold Funds / Gold Savings Fund :

Gold fund is a Fund of Fund which will invest in Gold ETFs on behalf of you. Best part here is that you do not require holding any demat a/c here. Then how to invest in Gold Mutual Funds? Just like investing in other mutual fund schemes. As this is like any other mutual fund scheme, SIP investment in gold is possible through these gold funds. Still buying Gold fund of fund is little expensive option, as you have to pay 1) Annual management charges for the underlying Gold ETF 2) Annual management charges of Gold FOF .

Funds charge about 0.5 – 2 % as fund management charges annually.

They invest in gold mining companies / shares and therefore are based on profitability patters and manufacturing cycles of these companies

Physical gold :

Gold coins , Bars , Jewellery :

Jewellery can be bought from any reputed jeweler while banks sell gold coins and bars now. The single-most important thing to check is the product’s ‘Assay Certification’, indicating quality. When buying coins and bars, make sure the product is in a tamper-proof pack that prevents damage during transit. If you decide to buy gold coins or bars worth over Rs 50,000, banks will ask for PAN card details and identity proof, while a jeweler does not.

HALLMARK AND CERTIFICATION

BIS certified jewellers can get their jewellery hallmarked from any BIS recognised Assaying and Hallmarking Centre.

A Hallmark consists of five components-BIS mark, the Fineness number (corresponding to given caratage, see table), Assaying and Hallmarking Centre’s mark, Jeweller’s identification mark and year of marking (in a code decided by BIS-A for the year 2000, B for 2001 and J for 2008). The marking should be embossed on the product.

958 Corresponding to 23 Carat

916 Corresponding to 22 Carat

875 Corresponding to 21 Carat

750 Corresponding to 18 Carat

585 Corresponding to 14 Carat

375 Corresponding to 9 Carat

The Indian gold coin, minted in India and sold by MMTC and select banks, is available in denominations of 5/10/20 grams. The coin will be of 24 karat (999 fineness) purity and wrapped in tamper-proof packaging. It also has anti-counterfeit features such as the one in currencies plus a hallmark certification that makes it more reliable than gold that is bought from the next-door jeweller.

Drawbacks:

Subject to wealth tax. You need to pay 1% of the value of gold you hold each year if your total wealth is above Rs.30 lakh

High making/damage charges – This is one major disadvantage if you buy gold as ornaments. Indian jewel makers charge anywhere between 10-20% as damage charges. If it is antique jewellery it is as high as 65%. So if you’re investing Rs.3,00,000 you can lose 40-60k at the beginning itself

Questionable purity – You can’t possibly predict the purity of gold especially from smaller jewellers . You have to believe what the jeweler says. And if the quality is low, you get less money when you sell it. Storage/Safety – Physical gold has to be guarded by you. You need to pay for storage in lockers at home/bank. There is also the possibility of theft. Considering that, a single loot can leave you stripped with big portion of your wealth.

Short/long term capital gains period is 3 years. That is, if you sell gold in less than 3 years after buying, you need to pay capital gains tax which is 10% or 20% without/with indexation –

| Details | Physical Gold Bullion | Gold Jewellery | Gold ETF | Gold Savings fund |

| Asset Type | Coins, Bars , biscuit | Any gold ornament | Gold ETF MF – 1 unit = 1 gm gold | A super fund which invests in other gold instruments |

| Gold Purity | 99% subject to tests | 22 carat , 92% subject to test | Tested and stored as 99.5% pure bullion | Investment in e-gold |

| Where to buy | Banks , jewellers | Jewellers | Exchange – NSE/ BSE | MF online or agents |

| SIP options ? | NO | NO | NO | Yes |

| Storage options | Home, bank lockers | Home, lockers | Gold is held in a mass storage with regular audits & security | No physical gold involved |

| Entry charges | 4 – 6 % | Making charges 7-20% | Demat & brokerage | Fund management charges ~ 2% |

| Recurring charges | Locker rent | Locker rent | Fund management fee of 1% | Fund management charges ~ 2% |

| Exit charge | 2-6% charges of the buying price of that day | Jewellers offer 4-8% lesser than buy rate of the day | Broker commission | Usually 1.5-2% exit load if less than a year |

| Liquidity | Fairly liquid | Fairly liquid | High liquidity , T+2 days | Highly liquid , T+2 days |

| Capital gains – long term | 10% without indexation ,20% with indexation | 10% without indexation ,20% with indexation | 10% without indexation ,20% with indexation | 10% without indexation ,20% with indexation |

| Wealth Tax | Liable to wealth tax of 1 % a year for excess of Rs.30 lakh | Liable to wealth tax of 1 % a year for excess of Rs.30 lakh | Not Liable | Not liable |

Tax benefits

Gold ETFs have an edge over e-gold . For gold ETFs, one year is considered as the long term; it is three years for e-gold. Also, egold attracts wealth tax.

“E-gold is treated like physical gold and qualifies for long-term capital gains benefits if held for three years or more. However, gold ETFs qualify for long-term capital gains treatment after being held for just one year. Gold ETFs are considered financial assets and hence are exempt from wealth tax, which is not the case with e-gold,” says Nayak of Centrum Broking.

Gains from gold ETFs, if sold within one year, are taxed according to the person’s tax slab and at 20 per cent (after indexation) if sold after a year. Gains from e-gold, if it is sold within three years, are taxed according to the tax slab and at 20 per cent (after indexation) if sold after three years.

What the future holds for vested parties

The diversity of gold-backed and gold-related products means that gold can be used to enhance a wider variety of individual investment strategies and risk tolerances. Investors also make use of gold’s lack of correlation with other assets to diversify their portfolios and hedge against currency risk.

Is Gold the new asset to invest in 2016?

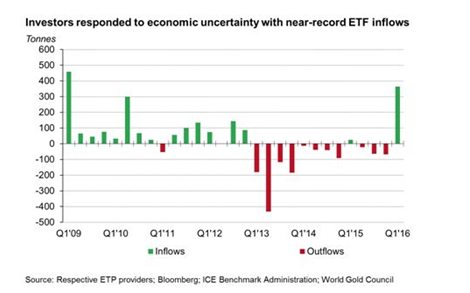

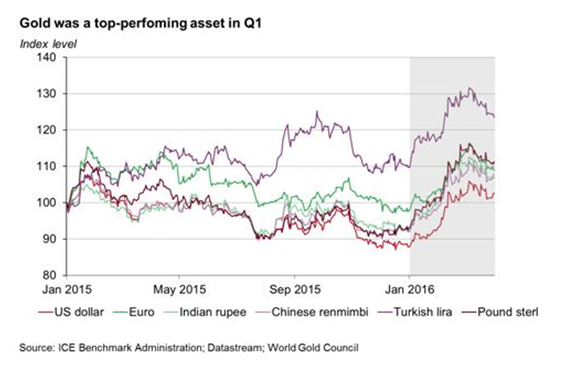

Gold staged a spectacular rally in the first quarter of this year, rising 17% in US dollar terms – its best performance in almost three decades. The return on gold significantly outperformed other major stock, bond and commodity indices. Its believe that these factors will continue to support both investment and central bank demand in the coming quarters. Gold demand reached 1,290 tonnes Q1 2016, a 21% increase year-on-year, making it the second largest quarter on record. This increase was driven by huge inflows into exchange traded funds (ETFs) – 364t – fuelled by concerns around the shifting global economic and financial landscape.

Higher prices and industrial action in India pushed global demand for jewellery down (-19%), while total bar and coin demand was marginally higher (+1%). Central banks remained strong buyers, purchasing 109t in the quarter. Total supply increased 5% to 1,135t. Hedging by producers (40t) supported an increase of 56t in mine supply, although countered by a marginal decline in recycling.

Combined with an analysis from past bull-bear cycles, this suggests entry to a new bull market for gold.

–Sneha Ramamurthy

Research Desk- Dilzer Consultants Pvt Ltd

- http://profit.ndtv.com/news/your-money/article-investing-in-gold-7-facts-you-should-know-317318

- https://en.wikipedia.org/wiki/Gold_reserve

- http://finmin.nic.in/swarnabharat/sovereign-gold-bond.html

- http://economictimes.indiatimes.com/articleshow/49597963.cms?utm_source=contentofinterest&utm_medium=text&utm_campaign=cppst

- http://nsegold.com/know-gold-etf.php

- http://www.moneycontrol.com/news/gold/should-you-buy-gold-jewellery-or-gold-etf_1811841.html?utm_source=ref_article

- https://rbi.org.in/scripts/NotificationUser.aspx?Mode=0&Id=10084

- http://economictimes.indiatimes.com/articleshow/52159783.cms?utm_source=contentofinterest&utm_medium=text&utm_campaign=cppst