Book an Appointment

Client Login

International Investing

INA 200002239

SEBI Registered Corporate Advisor

HOME

ABOUT US

OUR SERVICES

KNOWLEDGE CENTER

FINANCIAL HEALTH

NRI CORNER

MEDIA

CAREERS

CONTACT US

FAQS

Finance Planning Login

Client Login

International Investing

Best SEBI Registered Investment Advisor in Bangalore |Dilzer Consultants

We Promise to help you plan better.

Fill up this simple form to speak to a certified financial planner.

Get in Touch

Reload

Media

Published by deccanherald.com : GIFT City's investment opportunities for overseas clients

Read More

Published by deccanherald.com : Get smart on your loan prepayment

Read More

Published by outlookindia.com : Planning for Retirement: Smart Strategies For Every Stage of Life

Read More

Published by Economictimes : Investing in 2025: Six wealth management trends to watch out for

Read More

Published by outlookmoney.com : Market Euphoria And Herd Mentality: A Risky Combination In India

Read More

Published by moneycontrol.com : Here's how NRIs can navigate global trends to make most of their India investments

Read More

Published by Deccan Herald : Surrender value vs paid-up value: Know the key differences

Read More

Personal Fianance TV with Mbubina Kapasi

Read More

Published by Deccan Herald : Estate planning & legacy preservation for smooth transition of wealth

Read More

Published by financialexpress.com : Smart investment choices for NRIs: Leveraging global markets

Read More

Published by economictimes.indiatimes.com : How to build Rs 1 crore nest egg: A guide to SIP calculators

Read More

Published by moneycontrol.com : What’s the adequate number of mutual funds an investor should hold in a portfolio?

Read More

Published by livemint.com: Here's how you can read different mutual fund ratios when picking a fund

Read More

Published by livemint.com: Healthcare in retirement: How to insure yourself amid rising medical costs

Read More

Published By: Outlookindia.com...... Maximize Your #Retirement #Portfolio Growth! Planning for retirement? Discover key strategies to boost your portfolio and secure your financial future.

Read More

Published By: Outlookindia.com...... Learn how to maximize your income and minimize your taxes during #retirement. —an article by @Dilshad Billimoria (Certified Financial Planner) in Outlook India.

Read More

Estate planning isn't just for the wealthy—it is for anyone who wants to secure their assets and provide for their loved ones. Discover how effective estate planning can help you safeguard your legacy and ensure your wishes are honoured.

Read More

Published By: deccanherald.com..... Learn how to minimize your tax liability with expert strategies! Whether you're a salaried employee or a business owner, this article has valuable tips to help you keep more of what you earn

Read More

Published By: deccanherald.com..... A 360 Degree approach to managing portfolio risk

Read More

Published By: financialexpress.com..... How ESG Investing can make a social impact on your investment journey.

Read More

Published By: financialexpress.com..... Philanthropy and social investing: How to make a difference with your money

Read More

Published By: Mint..... Here’s a checklist for individuals moving overseas

Read More

Published By: Mint..... Investments in India: How moving to the US changes your tax compliance

Read More

Published By: outlookmoney.com.... Women Advisors Are Better Listeners And More Empathetic

Read More

Dilshad Podcast discussion with Anupam Gupta IVM Podcast Jan23 on Investments Financial Planning and Risk Management

Read More

Dilshad's Interview with Mint Newspaper on SEBI RIA Guidelines and Registered Investment advisors

Read More

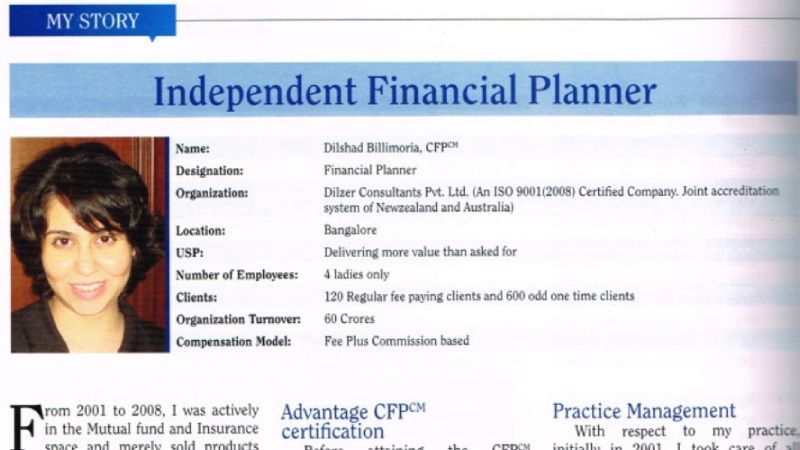

Dilshad's Journey as a Financial Planner and Investment Advisor

Read More

Women and Investing

Read More

Filling the gaps in the Financial Plan

Read More

CNBCTV18 on Retirement Planning for Women

Read More

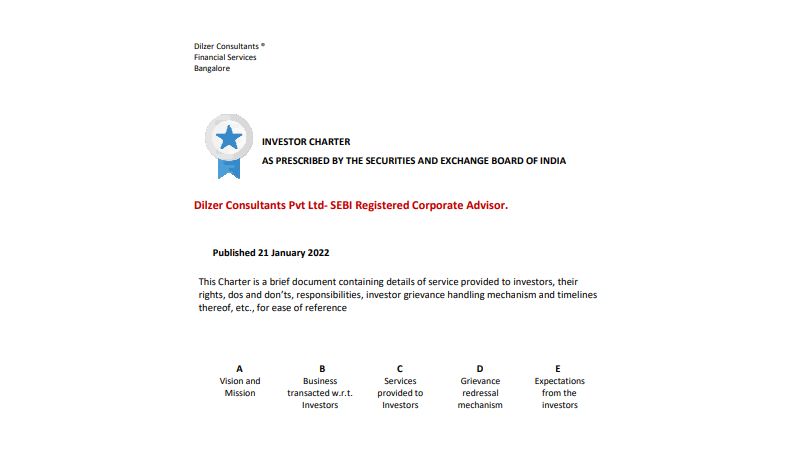

Investor Charter

Read More

What not to overlook in an Health Insurance Policy

Read More

Assessing Risk Tolerance, Risk Capacity, Risk Required

Read More

Sumaira Abdi CNBC TV 18 with Dilshad Billimoria

Read More

Portfolio Building Asset Allocation and Portfolio Rebalancing

Read More

Money Control Personal Finance. The when why and how of Portfolio Re-balancing.

Read More

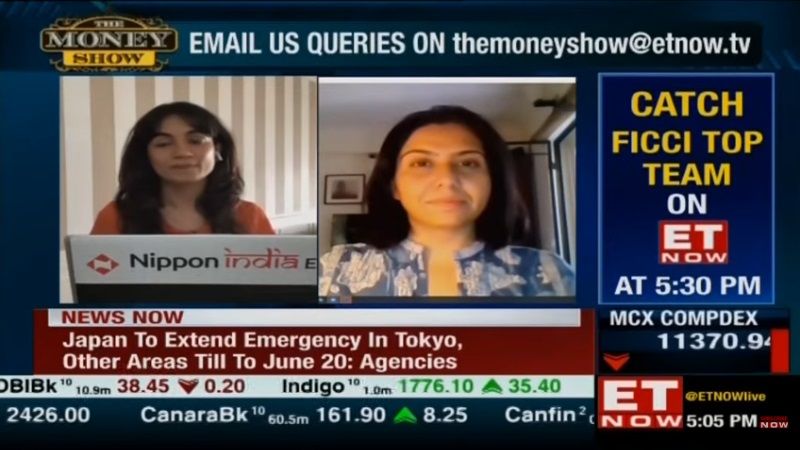

ET Now - The Money Show

Read More

What does a Financial Plan cover- Money Control

Read More

Money 9 TV : How to Plan your finances- World Financial Planning Day 6 October 2021

Read More

Money9 Finance Helpline

Read More

Environmental Social and Governance (ESG) Investing

Read More

Consider these seven steps to generate an Emergency fund for a rainy day

Read More

Ideal time to Re balance Portfolio and Mid and Small Cap Portfolio

Read More

#Covid19 Prep for 2nd Economic Fall out

Read More

The Global Analyst Magazine- Wealth Management Outlook 2021

Read More

ET NOW How to teach healthy money habits to your kids? | The Money Show

Read More

Dilshad in Outlook Money on both spouses included in discussions

Read More

Dilshad in MINT on Investment Guidelines to follow in the current uncertainty

Read More

What are the tax implications of receiving an Inherited Property

Read More

Insurance World, Jan 2006, Mumbai page 23

Read More

Dilshad Financial Planning Standards Board

Read More

E Book: Secrets of Top Financial Planners_Dilshad Billimoria

Read More

Annual goal review and its importance

Read More

Double indexation benefit on FMPs

Read More

12th Anniversary for Dilzer Consultants

Read More

Checklist for home loan buyers

Read More

Plot or a house?

Read More

Investors seek advice and want their financial advisors to be in touch with them

Read More

Financial Planning Standards Board of India Dilshad Billimoria July 2014 Insurance Regulation and Change

Read More

Financial Planning Standards Board of India Journal comments by Dilshad Billimoria Oct 2013

Read More

Outlook Money Feb 2014 on Budgeting with Dilshad Billimoria

Read More

Dilshad Billimoria speaks in Outlook Money September 2014 on Financial Planning for Single Women

Read More

India’s Accredited Best Financial Planners with Dilshad Billimoria

Read More

Dilshad writes in Mint about which is the best way to reduce home loan burden.

Read More

Dilshad Billimoria comments in Mint

Read More

Dilshad comments in Mint on “lessons financial gurus missed when they were young”

Read More

Dilshad Billimoria writes in Mint on the importance of Savings for children and teaching them the value of money

Read More

Budget 2015: Expectation from the Salaried Class. Dilshad writes in Dalal Times.

Read More

Dilshad writes in Dalal Times

Read More

Interview of Dilshad Billimoria with thefundoo.com

Read More

Bullet Proof Your Health- COFP FP Pulse Article by Dilshad Billimoria

Read More

A Financial Plan is a blue print to your financial goals- By Dilshad Billimoria in Mint

Read More

Understanding the nuances of India’s Fiscal policy- By Dilshad Billimoria

Read More

Dilshad comments in Outlook Money on Financial Freedom- 15 August 2015

Read More

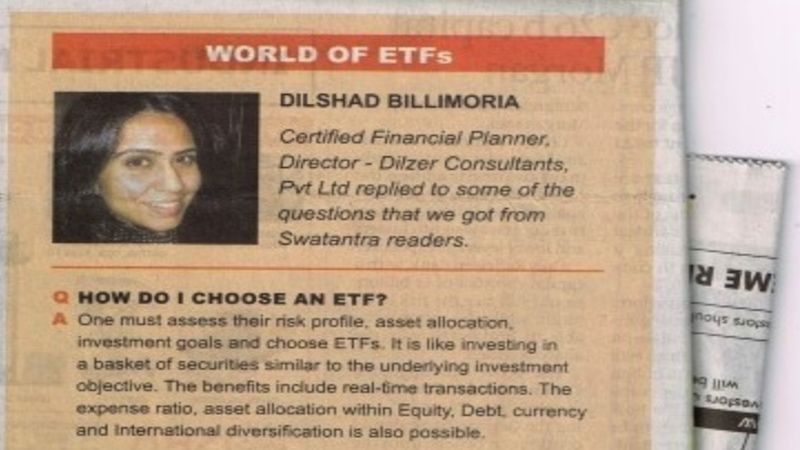

Dilshad responds to readers queries on Exchange Traded Funds- Business Line – 9 Sept 2015

Read More

Have you been mis-sold an insurance policy- Here's what you can do- written by Dilshad Billimoria in Economic Times - 15 Sept 2015

Read More

Are you under insured- find out how much insurance cover you really need- Dilshad comments in Economic Times – Wealth

Read More

Economic Times- Featured as one of the best wealth managers in the country

Read More

Should you pay fees to your investment advisor and why?

Read More

Bitcoins- the future of Money

Read More

How to choose the right health insurance plan

Read More

Woman 2.0 The empowered one

Read More

Should you hire an expert to manage your money?

Read More

Dilshad Billimoria on #ETNow #TheMoneyShow

Read More

What is debt refinancing and how will it help in reducing your EMI?

Read More

Is Real Estate a good investment for realizing your financial goals?

Read More

ET Now- The Money Show 9 April 2019

Read More

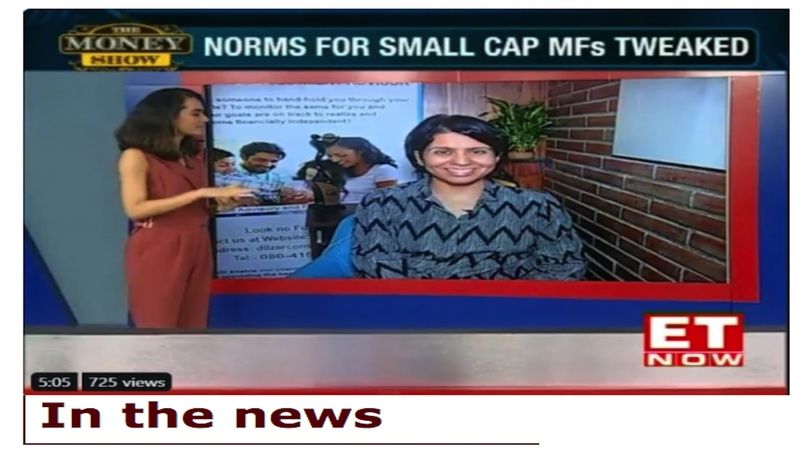

SEBI Categorization Money Show ET Now 6 September 2019

Read More

Award from White Page India – Dilshad “India’s Most Admired Financial Advisor” September 2019

Read More

White Page India Powered by India Today Awards

Read More

Prenuptial agreements: building a safety net around assets

Read More

Women ahead: How independent wealth managers are making gender distinctions meaningless

Read More

Financial planners focus spotlight on skills

Read More

How best to reduce the burden of home loan prepayment

Read More

What one can do with unwanted and mis-sold insurance policies

Read More

Accelerate your way to financial independence

Read More

Advisor Speak. The Future of Money

Read More

Watch Dilshad on ET Now, answering queries from investors

Read More

Ever thought about what will happen to your loved ones in your absence?

Read More

Millennials Money Mistake – 3 Major Solutions

Read More

We Promise to help you plan better.

Fill up this simple form to speak to a certified financial planner.

Get in Touch

Reload